How The VA Loan Works

VA home loan is a mortgage made by a private lender (bank/mortgage company/credit union) that’s backed by the U.S. Department of Veterans Affairs (VA). The VA doesn’t lend the money directly. It provides a loan guaranty that reduces the lender’s risk, which is why VA loans often come with flexible terms for eligible Veterans, active-duty service members, and Eligible surviving spouses.

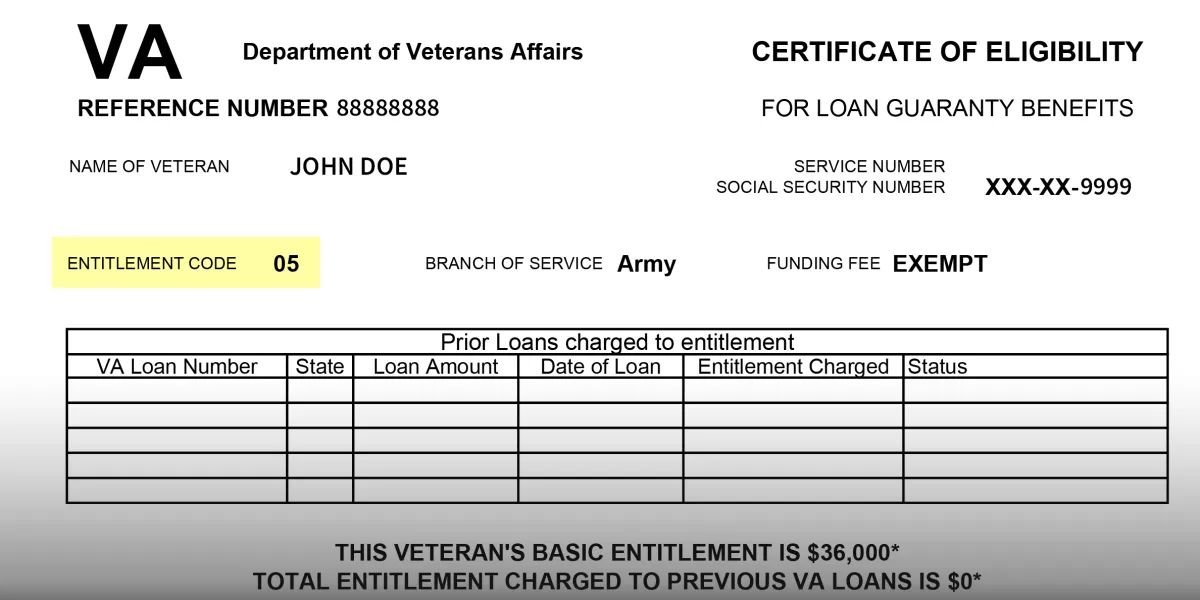

VA Loan Entitlement

Entitlement is your available VA benefit, the amount of guaranty the VA can provide on your behalf. Your Certificate of Eligibility (COE) shows whether you have entitlement available and how much (if any) has been used before.

How Entitlement is Restored is Restored

1. Sell the home and the VA loan is paid in full (most common)

2. Refinance out of the VA loan into a non-VA loan (VA loan paid off)

3. A qualified veteran assumes your VA loan and substitutes their entitlement (so yours is freed up)

4. One-time restoration: you pay off the VA loan but keep the home (allowed once)

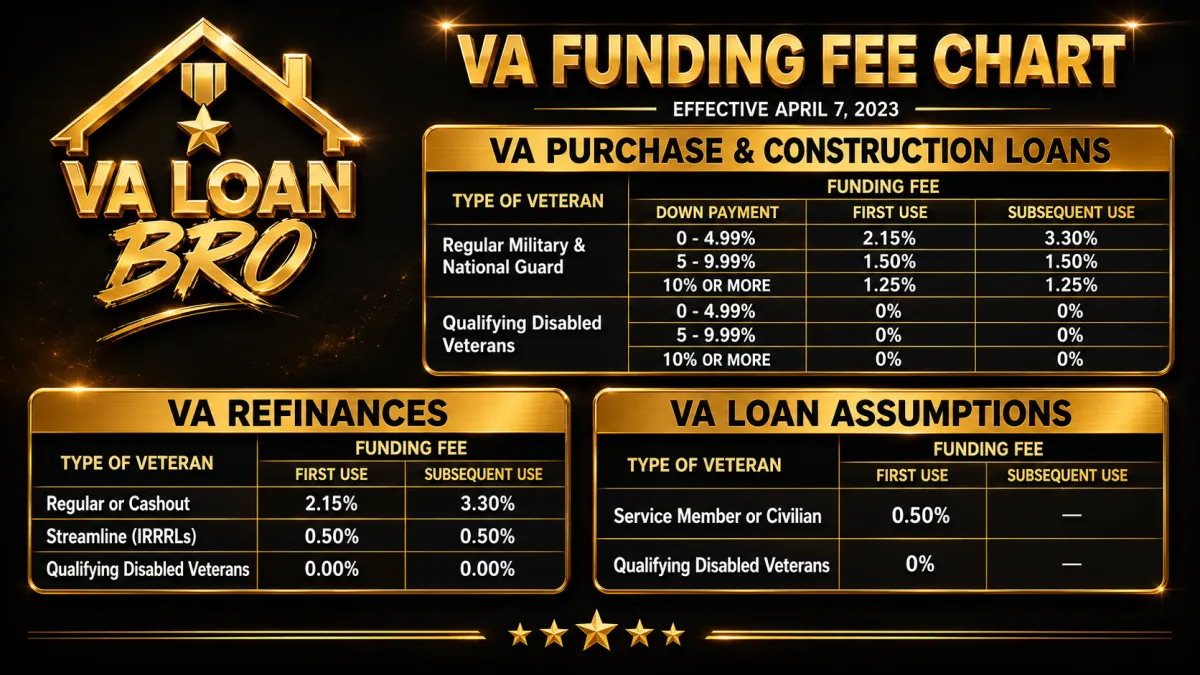

VA Funding Fee

1. The VA funding fee is a one-time charge on most VA loans that helps keep the VA home loan program running (so it can offer benefits like $0 down and no monthly mortgage insurance).

2. It’s calculated as a percentage of the loan amount (not the home price).

3. The percentage depends on things like first-time vs. repeat use, down payment amount, and loan type.

4. You can often finance it into the loan (roll it in) instead of paying it out of pocket at closing.

5. Some borrowers are exempt, commonly certain Veterans receiving VA disability compensation (and other eligible categories).

If you’re not exempt, another party can pay it (seller, lender, or even a family gift), depending on how your deal is structured.

Key Benefits of The Va loan

NO down payment requirement

VA loans offers service members the ability to finance up to 100% of the purchase price of a home. Other loan types such as conventional and FHA loans may require a minimum down payment.

NO monthly mortgage insurance (PMI)

VA loan does NOT require monthly mortgage insurance which is an extra monthly fee that usually comes with a conventional loan when you put less than 20% down. It protects the lender in case the borrower stops making payments. VA loans often have lower monthly payments compared to other loan types due to this.

Competitive Interest rates

Because the VA guarantees a portion of the loan, VA loans often come with more competitive (sometimes lower) interest rates than comparable conventional or FHA financing.

Lifetime benefit (use it more than once)

Your VA home loan benefit can be used multiple times over your lifetime (as long as you have sufficient entitlement).

Assumable mortgage

VA loans are generally assumable meaning a future buyer may be able to take over your existing VA loan (including the rate) if they qualify and the servicer approves the assumption. This can be a big resale advantage in a high-rate market.

No prepayment penalty

VA borrowers have the right to pay off the loan early without a prepayment penalty.

Allows up to 4% in sellers concessions on top of seller paid closing costs

VA Interest Rate Reduction Refinance Loan (IRRRL)

Key Features of a VA IRRRL

• No appraisal required in most cases

• No income or employment verification required

• No out-of-pocket costs in many situations (costs can often be rolled into the loan)

• Faster and simpler process compared to a traditional refinance

• Must result in a net tangible benefit to the borrower (lower rate, lower payment, or more stable loan)

What Is a “Net Tangible Benefit”?

The VA requires that the refinance clearly benefits the veteran. This usually means:

• Lowering the interest rate

• Reducing the monthly payment

• Moving from an adjustable rate to a fixed rate

• Improving long-term financial stability

NOTE: This rule is in place to protect veterans from unbeneficial refinancing.

Who Typically Benefits Most from an IRRRL?

A VA IRRRL may be a good option if you:

• Currently have a higher interest rate than today’s market

• Want to lower your monthly payment

• Have an adjustable-rate VA loan and want a fixed rate

• Prefer a refinance with minimal documentation and faster closing

Seasoning Requirements

Before using a VA IRRRL, the following must be true:

• At least 210 days have passed since your first mortgage payment due date

• You’ve made at least 6 monthly payments on your current VA loan

Occupancy Requirement

You do not need to currently live in the home

• You must have lived in the home previously

• Investment properties are allowed if prior occupancy can be verified

Still have questions about your benefit?

Thank you for choosing us. We are dedicated to helping you achieve your homeownership goals with personalized service and expert guidance. For more information or assistance, feel free to reach out to us anytime!

quick info

+1 (949) 813-4713

Your VA Loan Advisor

Bryce Pierce